Credit card payments have become essential for modern commerce which allows businesses to accept fast, convenient, and secure transactions both online and offline.

While payments appear to happen instantly to customers, the actual credit card transaction process has many steps happening behind the scenes before funds are deposited into a merchant’s account.

Understanding how long credit card transactions take to process is essential for businesses that rely on steady cash flow, accurate financial planning, and efficient payment management.

The actual credit card processing timeline involves authorization, batching, clearing, and settlement. Where every phase involves communication between the issuing bank of the customer, the card network, the payment processor, and the merchant account provider.

Although most transactions are completed within 1-3 business days, processing times can differ based on factors such as the payment method used, the merchant’s industry, bank policies, weekends, holidays, and potential fraud reviews.

For business owners, if there is delay in payment processing can affect cash flow, stock purchasing, and overall operations. Hence, it has become essential for businesses to select a reliable payment provider.

Modern payment providers help AcePay help businesses streamline the credit card payment process with advanced technology, secure transaction handling, and faster funding options which helps to improve operational efficiency.

Through this blog, we will walk you through each phase of credit card transaction processing, explore the factors which affect settlement times, discuss common reasons for payment delays, and offer practical tips that help businesses to improve their payment operations.

Merchants by understanding the complete process can manage customer expectations, improve financial planning, and ensure a smooth payment experience for both businesses and their customers.

Also Read: Credit Card Processing Fees

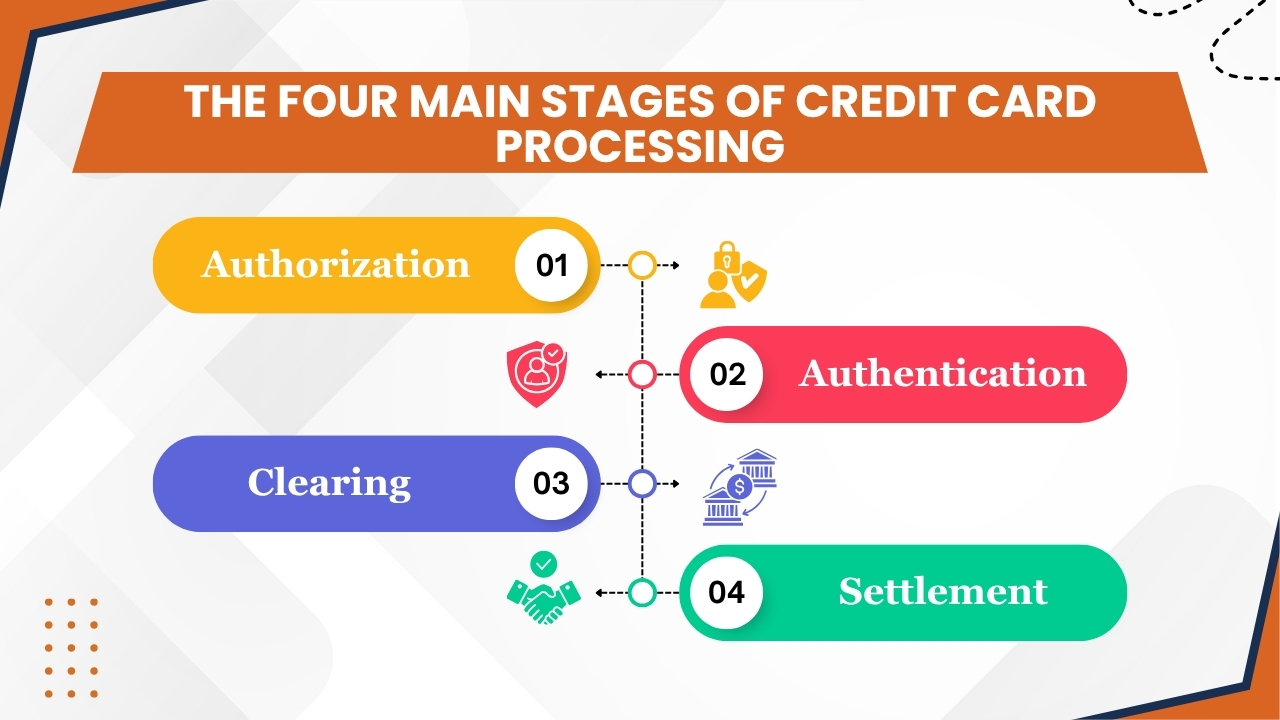

The Four Main Stages of Credit Card Processing

Understanding the time taken for credit card transactions begins with understanding the four crucial phases involved in every payment.

Although the entire process may appear to be happening instantaneously to customers, there are several important phases behind the scenes before funds are deposited into a merchant’s account.

1. Authorization

Authorization is the first stage of the credit card processing cycle. It begins when a customer swipes, taps, inserts, or enters their card details online, then the payment system of the merchant sends a transaction request through the payment processor and card network to the issuing bank.

The issuing bank then checks the transaction by checking the available credit limit, card validity, account status, security credentials, and potential fraud indicators.

And if everything meets the required criteria, the bank then approves the transaction and places a temporary hold on the necessary funds.

This stage usually takes only a few seconds which allows customers to receive near-instant approval. But, authorization does not transfer money to the merchant instead it simply reserves the fund for the transaction.

2. Authentication

Authentication works as an additional security layer designed to check the identity of the cardholder and reduce the risk of fraud transactions. This step is crucial for online and card-not-present transactions.

It may include CVV verification, Address Verification Service (AVS) checks, one-time passwords (OTP), two-factor authentication, and 3D Secure protocols.

In most cases, authentication happens simultaneously with authorization and does not noticeably affect transaction speed. However, when a transaction requires additional verification, processing times may experience minor delays while extra security checks are completed.

3. Clearing

After authorizing a transaction, the next stage is clearing. In this phase, transaction details are gathered, verified, and prepared for settlement.

Here, card issuers, acquiring banks, and payment networks, review transaction data, match transaction details, and coordinate settlement processing.

Most merchants submit authorized transactions in batches at the end of the business day instead of processing each transaction individually.

As a result, the timing of such batch submissions can highly affect how quickly a transaction progresses to the next stage.

4. Settlement

The final stage of the credit card transaction process is settlement. In this stage, funds move from the issuing bank through the card network to the acquiring bank, which then the funds are deposited into the merchant’s account.

Applicable processing fees are deducted before the funds become available. Based on the payment processor, banking schedules, weekends, holidays, and merchant account settings, settlement usually happens in 1-3 business days.

Once settlement is completed, the transaction is fully processed and the merchants get access to the funds.

Also Read: How Restaurant Credit Card Processing Works Step By Step

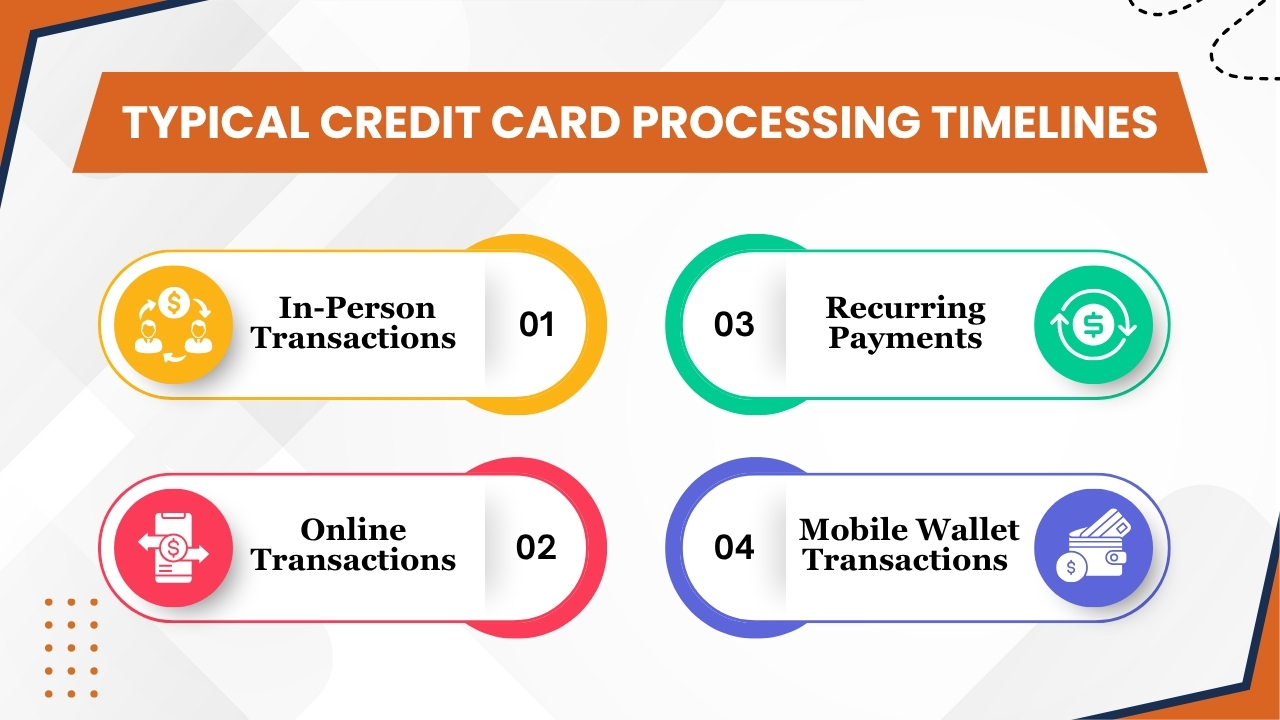

Typical Credit Card Processing Timelines

Though every credit card transaction has the same general processing phases, the amount of time required to complete the process can be different based on how the payment is made.

Due to factors like fraud risk, verification requirements, payment methods, and processor capabilities all affect how quickly merchants receive their funds.

Below are the most common transaction types and their usual processing timelines:

1. In-Person Transactions

Card-present transactions are generally the fastest and most efficient type of credit card payment. As the customer physically provides the card during the transaction these payments have a lower risk of fraud and require fewer verification checks.

Common examples include:

- EMV chip card payments

- Contactless tap-to-pay transactions

- Mobile wallet purchases at physical terminals

- Traditional magnetic stripe card swipes

When a person initiates an in-person transaction, authorization usually happens within a few seconds. The issuing bank quickly verifies the card details, available credit, and security details before approving the payment. Once approved, the transaction is added to the merchant’s batch for processing.

Most payment processors submit batches at the end of every business day. After the batch is transmitted, the transaction moves through clearing and settlement.

In most cases, merchants receive access to their funds within 1-2 business days. Businesses using advanced processors or same-day funding programs may receive deposits even faster.

Because of lower risk of fraud and smooth verification requirements, card-present transactions usually experience the shortest overall processing timelines.

2. Online Transactions

Online payments are also known as card-not-present transactions, usually requiring additional security checks compared to in-person purchases.

As the physical card is not available for verification, payment processors and issuing banks perform extra verification processes to reduce fraud and protect both merchants and consumers.

Additional security measures often include:

- Address Verification Service (AVS)

- CVV verification

- Fraud detection screening

- Risk analysis algorithms

- 3D Secure authentication

- Behavioral monitoring tools

Although authorization still occurs within seconds in most cases, these additional checks can occasionally introduce minor delays. Transactions that cause fraud alerts may undergo manual review before approval.

After authorization, online payments move through the standard clearing and settlement process. Most e-commerce businesses need funds within 1-3 business days, based on their payment processor and banking relationships.

High-risk industries or merchants with high chargeback rates may experience longer settlement periods. Despite all these factors, modern payment technology has highly improved the speed of online processing which allows most transactions to be completed efficiently.

3. Recurring Payments

These types of payments are mostly used for subscription services, memberships, software-as-a-service(SaaS) platforms, streamlining services, and automated billing programs.

As payment details of customers are securely stored and verified during the initial transaction, recurring charges often move through the authorization process more smoothly than first-time purchases.

Examples of recurring billing include:

- Subscription memberships

- Monthly software fees

- Streaming service payments

- Automated utility payments

- Fitness club memberships

- Maintenance service agreements

Whenever a recurring payment is scheduled, the processor instantly submits the transaction on the designated billing data. As customer details have already been validated, authorization usually happens quickly and with less interruptions.

However, recurring transactions still proceed through clearing and settlement like any other payment. Merchants can usually expect settlement within 1-3 business days.

Delays may happen when a card has expired, available credit is insufficient, or account details have changed. Businesses that depend on recurring billing often benefit from automated account updater services that help to maintain uninterrupted payment processing and reduced failed transactions.

4. Mobile Wallet Transactions

Mobile wallet payments have become more popular in recent years because of the speed, convenience, and enhanced security that it offers. Many services such as Apple Pay, Google Pay, and Samsung Wallet are letting customers make purchases without physically providing a credit card.

Mobile wallet transactions offer several advantages:

- Tokenized payment credentials

- Enhanced encryption

- Biometric authentication

- Reduced fraud risk

- Faster checkout experiences

- Improved authorization success rates

As mobile wallet payments are usually considered as card-present transactions while used in physical stores, they often follow processing timelines as same as EMV chip and contactless card payments.

Authorization usually happens within seconds, and transactions are added to the merchant’s batch for end-of-day processing.

Settlement usually happens within 1-2 business days, based on processor capabilities and banking schedules. The advanced security features built into digital wallets help to reduce fraud activities and reduce declines that happen because of security concerns.

As a result, most businesses experience strong approval rates and efficient processing while accepting mobile wallet payments.

Overall, though transaction timelines may differ slightly based on payment method, most credit card transactions are authorized almost instantly and settled within 1-3 business days.

Understanding these timelines helps businesses to better manage cash flow, plan operations, and set realistic expectations for fund availability.

Also Read: Restaurant Credit Card Processing Companies for Small Businesses

Why Some Transactions Remain Pending

One of the most common concerns among consumers and merchants is seeing a credit card transaction listed as “pending”. A pending transaction indicates that the payment has been authorized by the issuing bank, but the transfer of funds has not been fully completed through the clearing and settlement process.

It means the bank has approved the purchase and reserved the necessary funds, but the transaction is still moving through the payment network before reaching the merchant’s account.

Pending transactions are a normal part of credit card processing and it does not necessarily indicate a problem. Most transactions remain pending for a short duration while payment processors, card networks, and financial institutions complete the required verification and settlement procedures.

Based on the circumstances, pending transactions usually clear within 1-5 business days.

Several factors can cause a transaction to remain in pending status:

- Merchant Batch Processing Schedules – Many businesses submit transactions in batches at the end of the business day instead of processing them individually.

- Fraud Review Procedures – Transactions indicated of having security concerns may undergo additional verification before settlement.

- Weekend and Holiday Transactions – Banks and payment processors may not process settlements on non-business days, which cause temporary delays.

- Bank Processing Delays – Different banks have different settlement schedules and processing times.

- Large Transaction Amounts – High-value purchases may require additional verification before funds are released.

- International Payments – Cross-border transactions usually involve multiple banks, currencies, and compliance checks that can extend processing times.

For merchants, a pending transaction indicates that the payment has been approved and is going through the normal processing cycle.

However, the funds are not yet available for use until settlement is completed. Businesses by understanding why transactions remain pending can help to manage cash flow expectations and provide the right information to customers who may have queries about their payment status.

Also Read: Payment Processing Solutions for High-Risk Businesses

Factors That Affect Processing Speed

Although most credit card transactions are authorized within seconds, the time required for funds to move from authorization to settlement can differ highly.

Several factors influence how instantly a transaction progresses through the payment ecosystem.

Understanding these factors helps businesses to improve the way they manage cash flow, anticipate potential delays, and select payment solutions which support faster funding.

1. Issuing Bank Policies

The issuing bank plays a major role in determining transaction processing speed. Every bank has its own risk management procedures, authorization protocols, and internal processing schedules. Before approving a transaction, the issuing bank verifies account information, available credit, card status, and potential fraud indicators.

Some banks use highly automated systems that can approve transactions almost instantly, while others may apply more extensive security reviews. High-value purchases, unusual spending patterns, or transactions from unfamiliar locations may trigger additional verification procedures. These reviews can temporarily slow authorization and settlement timelines.

Issuing bank policies may also influence how quickly transactions move through clearing and settlement. Some financial institutions process transactions multiple times throughout the day, while others operate on fixed schedules. As a result, identical transactions can settle at different speeds depending on the cardholder’s bank.

Key impacts include:

- Authorization review requirements

- Fraud monitoring procedures

- Internal settlement schedules

- Risk management policies

- Account verification processes

Because merchants have little control over issuing bank operations, understanding these factors helps explain why transaction speeds may vary between customers.

Factors That Affect Processing Speed

Although most credit card transactions are authorized within seconds, the time required for funds to move from authorization to settlement can differ highly.

Several factors influence how instantly a transaction progresses through the payment ecosystem.

Understanding these factors helps businesses to improve the way they manage cash flow, anticipate potential delays, and select payment solutions which support faster funding.

1. Issuing Bank Policies

The issuing bank plays a major role in determining transaction processing speed. Every bank has its own risk management procedures, authorization protocols, and internal processing schedules. Before approving a transaction, the issuing bank verifies account information, available credit, card status, and potential fraud indicators.

Some banks use highly automated systems that can approve transactions almost instantly, while others may apply more extensive security reviews. High-value purchases, unusual spending patterns, or transactions from unfamiliar locations may trigger additional verification procedures. These reviews can temporarily slow authorization and settlement timelines.

Issuing bank policies may also influence how quickly transactions move through clearing and settlement. Some financial institutions process transactions multiple times throughout the day, while others operate on fixed schedules. As a result, identical transactions can settle at different speeds depending on the cardholder’s bank.

Key impacts include:

- Authorization review requirements

- Fraud monitoring procedures

- Internal settlement schedules

- Risk management policies

- Account verification processes

Because merchants have little control over issuing bank operations, understanding these factors helps explain why transaction speeds may vary between customers.

3. Transaction Type

The type of transaction being processed has a direct impact on how quickly it moves through the payment system. Different payment methods have different levels of risk that affect the amount of verification required.

Card-present transactions usually process more quickly as the physical card is available at the point of sale. While the ability to verify the card through EMV chips, contactless technology, or magnetic stripe data reduces fraud concerns and simplifies authorization.

Examples of faster-processing transaction types include:

- EMV chip transactions

- Contactless payments

- Mobile wallet purchases

- In-store card payments

On the contrary, card-not-present transactions usually require additional security measures as the card is not physically available.

Examples include:

- E-commerce purchases

- Online subscriptions

- Phone orders

- Mail-order transactions

These transactions often involve extra verification procedures such as:

- CVV validation

- Address verification

- Risk scoring

- Behavioral analysis

- 3D Secure authentication

Due to additional checks being required, online transactions may experience longer processing times than in-person purchases. As businesses primarily operate online should account for these differences while estimating settlement timelines.

While estimating payment settlement timelines, online merchants should take these processing differences into consideration.

4. Fraud Prevention Reviews

Fraud prevention is a crucial component of modern payment processing. Banks, card networks, and payment processors continuously track transactions to identify suspicious activity and protect both merchants and consumers.

When a transaction raises fraud-related concerns, additional validation procedures may be necessary to continue processing.

Common triggers include:

- Unusually large purchases

- Multiple transactions in a short period

- Purchases from unfamiliar locations

- High-risk merchant categories

- Inconsistent customer behavior patterns

- Cross-border purchases

In most cases, these reviews happen automatically and are completed within seconds. However, transactions that need manual verification may experience longer delays.

Although fraud reviews can temporarily slow processing, they offer crucial protection against chargebacks, financial losses, and unauthorized transactions.

Advanced fraud detection systems help to balance both transaction speed and security by identifying genuine threats while reducing unnecessary disruptions to legitimate purchases.

Merchants can reduce fraud-related delays by implementing strong security practices, tracking transaction activity, and working with processors which offer advanced fraud prevention tools.

5. International Payments

Cross-border transactions usually need more processing steps than domestic payments. While a payment involves multiple countries, banks have to coordinate across different banking systems, frameworks, and currencies.

International transactions often require:

- Currency conversion

- Additional fraud screening

- Compliance verification

- Anti-money laundering checks

- Cross-border authorization reviews

- International settlement procedures

Each additional step increases processing complexity and may extend settlement timelines.

Currency conversion alone can introduce delays because exchange rates must be verified and applied before settlement can occur. Furthermore, international transactions frequently involve intermediary institutions that help facilitate payment transfers between countries.

Factors affecting international payment speed include:

- Country-specific banking regulations

- Currency exchange requirements

- Regional compliance standards

- International banking networks

- Cross-border fraud controls

As a result, international payments often take longer to settle than domestic transactions. Businesses that regularly serve international customers should anticipate slightly extended processing times and plan cash flow accordingly.

Also Read: Best Credit Card Processing Companies for Small Businesses

6. Weekends and Holidays

Banking schedules have a significant impact on settlement timing. While authorization systems often operate continuously, many settlement activities occur only during standard banking business days.

Transactions initiated on weekends or public holidays or public holidays may not enter the settlement process until the next business day.

This delay does not necessarily indicate a problem within the transaction; instead it reflects the operating schedules of banks and financial institutions.

Common scenarios include:

- Friday evening transactions settling on Monday

- Holiday purchases settling after banking operations resume

- Extended holiday weekends creating additional delays

- International holidays affecting cross-border payments

Merchants often notice increased settlement times during periods when banking activity is reduced. Although modern payment technology has improved processing efficiency, many financial institutions still depend on business-day settlement schedules.

Including weekends and holiday periods in financial planning helps businesses to better predict when funds will become available. To better manage expectations, businesses should include weekends and holiday periods in financial planning which helps businesses to better predict when funds will become available.

It is essential to understand these timelines which help to avoid any type of confusion and improve financial planning.

Ultimately, transaction processing speed depends on a lot of factors such as bank policies, processor technology, transaction characteristics, security reviews, international requirements, and banking schedules.

Understanding these factors, helps businesses to make informed decisions, improve payment operations, and select payment solutions which support faster, more reliable access to funds.

Conclusion

Understanding how long credit card transactions take to process is essential for businesses which depend on consistent cash flow and efficient payment operations.

Although most transactions are authorized within seconds, the complete journey from authorization to settlement usually takes 1-3 business days.

Different factors like transaction type, issuing bank policies, fraud prevention measures, international processing requirements, and banking schedules can all affect how quickly funds become available.

Understanding the four stages of credit card processing such as authorization, authentication, clearing, and settlement, lets business owners better anticipate payment timelines and manage their financial operations more effectively.

Knowing why certain transactions remain pending and what factors may cause delays can also help merchants to set realistic expectations and improve customer communication.

Selecting the right payment processing partner plays a crucial role in optimizing transaction speed and reliability. Modern providers like AcePay use advanced payment technology, smart transaction routing, strong security measures, and smooth settlement processes to help businesses process payments efficiently.

Due to faster funding, enhanced fraud protection, and improved transaction visibility can cause stronger cash flow management and a better overall payment experience.

While digital payments continue to evolve, businesses that understand the credit card processing lifecycle and invest in reliable payment solutions will be better positioned to improve operational efficiency, maintain healthy cash flow, and deliver a smooth payment experience for their customers.

If you still have any query about how long credit card transactions take to process then you may book a free demo at AcePay and we are more than happy to assist you.