In today’s quickly changing digital market, being able to accept electronic payments is essential for small and large businesses.

Whether you are running retail stores, restaurants, online merchants, and service providers, customers would expect the convenience to be able to make payment with credit and debit cards.

Though card payments can increase sales and improve customer satisfaction, it also has credit card processing fees that directly affect the profits of the company.

Hence, it is essential for businesses to understand these costs to improve operations, control expenses, and increase profits.

Every card transaction involves multiple parties, which includes issuing banks, card networks, acquiring banks, and payment processors.

As a result, merchants have to pay different payment processing fees such as interchange fees, assessment fees, and processor markups.

These charges often differ based on transaction type, card brand, industry, and pricing structure. Without having a clear understanding of merchant processing fees, businesses may end up paying more than necessary.

Modern payment providers like AcePay may streamline the payment acceptance process by delivering versatile payment options, clear pricing structures, and efficient tools which help businesses to manage transactions easily.

Despite the provider that businesses choose, it is essential to understand how credit card transaction fees are calculated is essential for making informed financial decisions.

This blog will walk you through a complete breakdown of credit card processing fees, by explaining the crucial components that make up processing expenses, the different pricing models available, common hidden charges, and practical strategies for reducing expenses.

When businesses have a deeper understanding of merchant services fees, payment processor pricing, and transaction costs, businesses can improve cash flow, increase profits, and choose payment solutions which support their long-term growth and operational goals.

What Are Credit Card Processing Fees?

It is the charges that businesses pay whenever customers use a credit card or debit card to complete a purchase. Such fees help to cover the expenses for authorizing, processing, securing, and settling electronic payment transactions.

Although card payments provide convenience and faster checkout experiences, behind multiple banks and payment service providers are involved in transferring funds from the account of the customer to the merchant.

For most businesses, credit card processing fees are between 1.5% and 3.5% of the transaction amount. But actual costs can be different based on the card type, payment method, industry, transaction volume, and processor pricing model.

For instance, if a customer spends $100 and the processing fee is 2.9%, the merchant would receive approximately $97.10 before any additional charges

Key facts about credit card processing fees include:

- Fees are charged on nearly every card transaction.

- Costs vary based on card type and transaction risk.

- Online transactions often have higher fees than in-person payments.

- Premium rewards cards typically carry higher processing costs.

- Multiple organizations share the processing fee.

Though the payment processors appear simple to customers, several parties work behind the scenes to ensure transactions are completed quickly, accurately, and securely.

The Three Main Components of Credit Card Processing Fees

Understanding credit card processing fees starts with knowing the three primary components which make up the total costs of every card transaction.

Though merchants often see a single charge on their processing statements, that fee is usually divided among several parties involved in facilitating the payment.

The three main components are interchange fees, assessment fees, and processor markups.

1. Interchange Fees

Interchange fees are usually the largest portion of a merchant’s credit card processing expenses. These fees are paid directly to the cardholder’s issuing bank.

The issuing bank provides the customer’s credit or debit card. Issuing banks charge interchange fees to compensate for the costs and risks associated with processing card transactions.

Interchange fees help cover several expenses, including:

- Fraud prevention and fraud-related losses

- Credit risk assumed by the issuing bank

- Customer rewards and loyalty programs

- Transaction authorization and processing costs

The amount charged in interchange fees varies depending on multiple factors, such as:

- Card type (credit, debit, rewards, business, or corporate cards)

- Merchant industry

- Card-present or card-not-present transactions

- Security measures used during processing

- Transaction value and risk level

Generally, interchange fees are between 1.15% to 2.70% of the transaction amount, plus a fixed fee per transaction. As these rates are established by card networks and issuing banks, merchants have little control over negotiating these costs.

2. Assessment Fees

Assessment fees are the fees charged by card networks such as Visa, Mastercard, Discover, and American Express.

Unlike interchange fees which directly go to issuing banks, assessment fees are paid directly to the card networks that support the operation and maintenance of their payment processing systems.

These fees help support:

- Payment network maintenance

- Security and fraud prevention systems

- Technology upgrades and innovation

- Brand management and operational expenses

- Global payment processing infrastructure

Although assessment fees are just a small percentage of total processing expenses, they are still a crucial part of every card transaction.

These charges are generally calculated as a small percentage of transaction volume and are non-negotiable as they are determined by the card networks themselves.

For merchants, assessment fees may seem small when compared to interchange fees, but they contribute to the overall cost of accepting card payments.

Understanding these fees can help businesses better understand their merchant statements and accurately verify their total processing expenses.

3. Processor Markup

The processor markup is the amount of processing fee retained by the payment processor or merchant services provider.

Unlike interchange and assessment fees which are transferred to banks and card networks, processor markups represent the revenue earned by the payment processing company.

Processor markups cover a variety of services, including:

- Transaction routing and authorization

- Merchant account management

- Payment gateway functionality

- Customer and technical support

- Reporting and analytics tools

- Security and compliance services

- Risk monitoring and management

One of the important aspects of processor markups is that they are negotiable. On the basis of transaction volume, industry, and business size, merchants may be able to secure lower rates or more favorable pricing structures.

Therefore it is essential for businesses to compare providers and carefully review processing agreements before signing a contract.

Variations by Transaction Type

Credit card processing costs can be different based on how a payment is accepted.

Different transaction types have different levels of risk, security requirements, and processing expenses that directly affect the fees that merchants will pay.

1. In-Person Transactions

In-person or card-present transactions mostly have the lowest processing fees as they have less risk. These transactions occur when customers physically offer their credit or debit cards and complete purchases using EMV chip readers, contactless payment terminals, or mobile wallets.

High security features associated with these payment methods help to reduce fraud and chargeback risks.

Usual in-person processing fees stay between 1.8% to 2.6% of the transaction amount, and a small flat fee like $0.08 per transaction.

Because of low-risk associated with such transactions, card present transactions often are the most favorable interchange rates available to merchants.

2. Online or Keyed-In Transactions

Online, phone, and manually entered transactions come under card-not-present transactions. Since the customer and card are not physically present during the purchase, these transactions often have a higher risk of fraud, identity theft, and chargebacks.

To compensate for this high risk, payment processors and card networks charge higher fees.

Businesses that operate online or accept payments over the mobile phone usually pay processing fees between 2.25% to 3.0%, plus a flat transaction fee of approximately $0.25.

Implementing fraud prevention tools and strong security measures can help to reduce risk and improve transaction approval rates.

3. Debit Card Transactions

Debit card transactions generally have the lowest processing costs among electronic payment methods. As funds are withdrawn directly from the customer’s bank account, issuing banks face less financial risk as compared to credit card transactions.Most debit card processing fees lie between 0.5% and 1.5% of the transaction value.

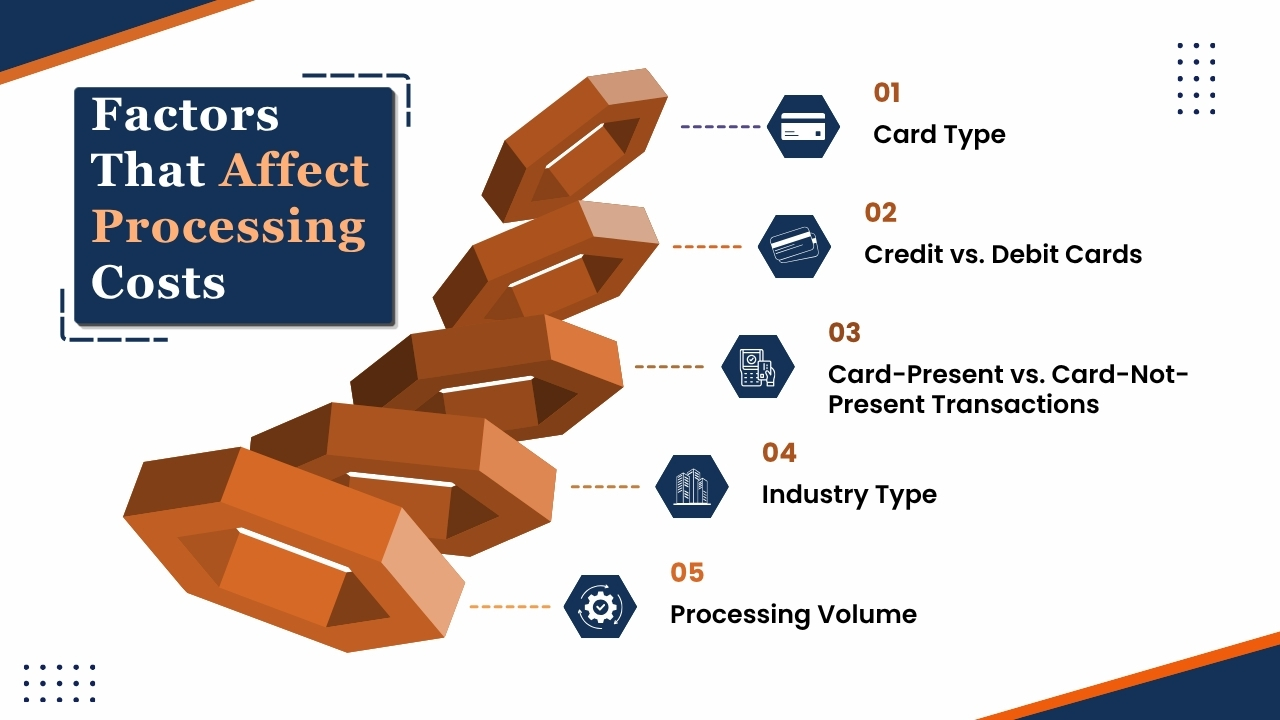

Factors That Affect Processing Costs

Several factors affect the credit card processing fees that businesses pay. Understanding these fees can help merchants to verify their expenses, and choose the right payment processors, and identify opportunities to reduce expenses.

1. Card Type

This type of card is used for a transaction significantly impacts processing costs. Standard debit and credit cards usually have lower fees, while premium rewards, travel, cashback, and business credit cards often have higher interchange rates.

Higher processing fees are often associated with these cards because issuing banks incur additional costs to provide cashback programs and other premium benefits to cardholders.

2. Credit vs. Debit Cards

Debit card transactions usually cost less to process when compared to credit card transactions. While debit purchases are often connected to a bank account of the customer, it involves lower risk for issuing banks.

While credit cards, on the other hand, need banks to increase credit and assume greater financial risks that usually cause higher processing fees.

3. Card-Present vs. Card-Not-Present Transactions

The method used to accept payments can also influence processing rates. In-person transactions using EMV chip readers, contactless payments, or mobile wallets usually qualify for lower fees as they provide more security and lower fraud risk.

Online, phone, and manually entered transactions are considered card-not-present payments and often have higher fees because of high exposure to fraud.

4. Industry Type

Certain industries are considered high risk by payment processors and card networks. Many businesses such as restaurants, subscription services, travel agencies, and e-commerce retailers face higher processing rates because of higher chargeback and fraud risks.

5. Processing Volume

Businesses that process large volumes of transactions often have higher chances of negotiations. Many payment processors offer reduced markups, custom pricing, or volume-based discounts to merchants with substantial monthly processing activity.

Common Credit Card Processing Pricing Models

1. Flat-Rate Pricing

Flat-rate pricing is one of the most popular and simple processing models among small businesses and startups.

Under this model, merchants pay the same price for every transaction despite the card type or transaction category. A common instance is 2.9% +$0.30 per transaction.

One of the benefits of flat-rate pricing is simplicity because business owners can easily predict processing costs as every transaction is charged at the same rate.

It is a straightforward pricing model that simplifies accounting, budgeting, and financial planning. Most modern payment service providers use flat-rate pricing as it is easy for merchants to understand instead of analyzing complex processing statements.

However, such convenience often comes with a cost. Large businesses with higher sales volumes may end up paying more than necessary because of low-risk transactions which are charged at the same rate as higher-risk transactions.

Merchants that process large numbers of debit card transactions or card-present payments may overpay when compared to other pricing models.

Although flat-rate pricing is a good option for smaller businesses who are searching for simple pricing structures, growing businesses often explore alternative pricing structures to reduce costs.

2. Interchange-Plus Pricing

Interchange-plus pricing is well known as one of the most transparent pricing models available.

Under this pricing model, businesses pay the actual interchange fee determined by card networks and issuing banks, plus a fixed markup charged by the payment processor.’

For instance, a processor may charge Interchange+0.20% +$0.10 per transaction.

One of the biggest advantages of interchange-plus pricing is transparency because merchants clearly see the amount of each fee going to the issuing bank and the amount of fee that is retained by the processor.

Such visibility makes it easier to compare providers, negotiate rates, and know the actual expenses of payment acceptance.

Interchange-plus pricing often results in lower overall processing expenses, specifically for medium and large businesses. While merchants pay the actual interchange rates, lower-risk transactions usually cost less than what they pay for flat-rate pricing.

Businesses with high processing volume can achieve sustainable savings over time.

The major disadvantage of pricing is complexity. Because merchant statements can be more difficult to understand because interchange rates vary based on card type, transaction method, and other factors.

Most payments experts consider interchange-plus pricing the most transparent and cost-effective option for businesses to process a high number of transactions.

3. Tiered Pricing

Tiered pricing organizes transactions into predefined categories based on perceived risk and processing characteristics. Usually, transactions are classified into three groups:

- Qualified transactions

- Mid-qualified transactions

- Non-qualified transactions

Qualified transactions receive the lowest rates and generally include standard debit card or basic credit card purchases processed under ideal conditions.

Mid-qualified transactions have higher fees and may involve rewards cards or manually entered payments. Non-qualified transactions receive the higher rates and often include premium rewards cards, business cards, or transactions with high risk factors.

The main attraction of tiered pricing is its simplicity in marketing. Payment processors often advertise attractive qualified rates which appear competitive at first glance.

However, most merchants find that a large percentage of their transactions come under the more expensive mid-qualified or non-qualified categories.

Hence, with tiered pricing makes it difficult for businesses to accurately predict expenses. Such lack of transparency may cause confusion while reviewing monthly statements, and some merchants may end up paying more than expected.

Businesses who are considered tiered pricing must carefully review contract terms and understand how transactions will be categorized before making a decision.

4. Subscription Pricing

Subscription pricing, sometimes known as membership pricing, has become popular among businesses that have high transaction volumes.

Instead of paying a higher markup on every transaction, merchants pay a fixed monthly subscription fee along with a small per-transaction markup.

Under this pricing model, businesses typically pay:

- A monthly membership fee

- Interchange and assessment fees

- A small fixed transaction fee or markup

The biggest advantages of subscription pricing is cost savings for businesses that process large numbers of transactions.

Though the profits of the processor happen primarily because of monthly membership fee rather than percentage-based markups, merchants can highly reduce overall processing expenses.

This pricing model is highly attractive for retailers, restaurants, wholesalers, and other businesses with substantial monthly sales volume.

It offers greater transparency than many traditional pricing structures. Merchants can clearly see the percentage of their costs goes toward interchange fees and what percentage goes to the processor.

However, this model may not be a good option for smaller businesses with lower transaction volumes. This monthly membership fee can exceed the savings generated from payment processing costs.

For this reason, businesses should carefully analyze their processing volume and compare total projected expenses before selecting a subscription-based pricing plan.

Hidden Fees Businesses Should Watch For:

While evaluating credit card processing costs, many businesses focus only on transaction costs and overlook additional charges which may appear on their monthly merchant statements.

These hidden fees can significantly increase the total expenses of payment processing and reduce overall profits if they are not carefully monitored.

Common hidden fees include PCI compliance fees, which cover security requirements for handling cardholder data, and monthly account fees charged simply for maintaining a merchant account.

Businesses may also encounter gateway fees for online payment processing, batch fees for settling daily transactions, and statement fees for generating account reports.

Other costs can arise from customer disputes and account management. For instance, chargeback fees are charged when customers dispute transactions, while retrieval request fees may apply when additional transaction documentation is requested.

Some processors also charge annual fees for maintaining account and early termination fees in case a merchant cancels a contract before its expiry date.

Although these annual charges may seem small individually, they can increase quickly over time. By regularly reviewing processing statements and understanding all applicable fees can help businesses to identify unwanted expenses and improve managing their overall payment processing expenses.

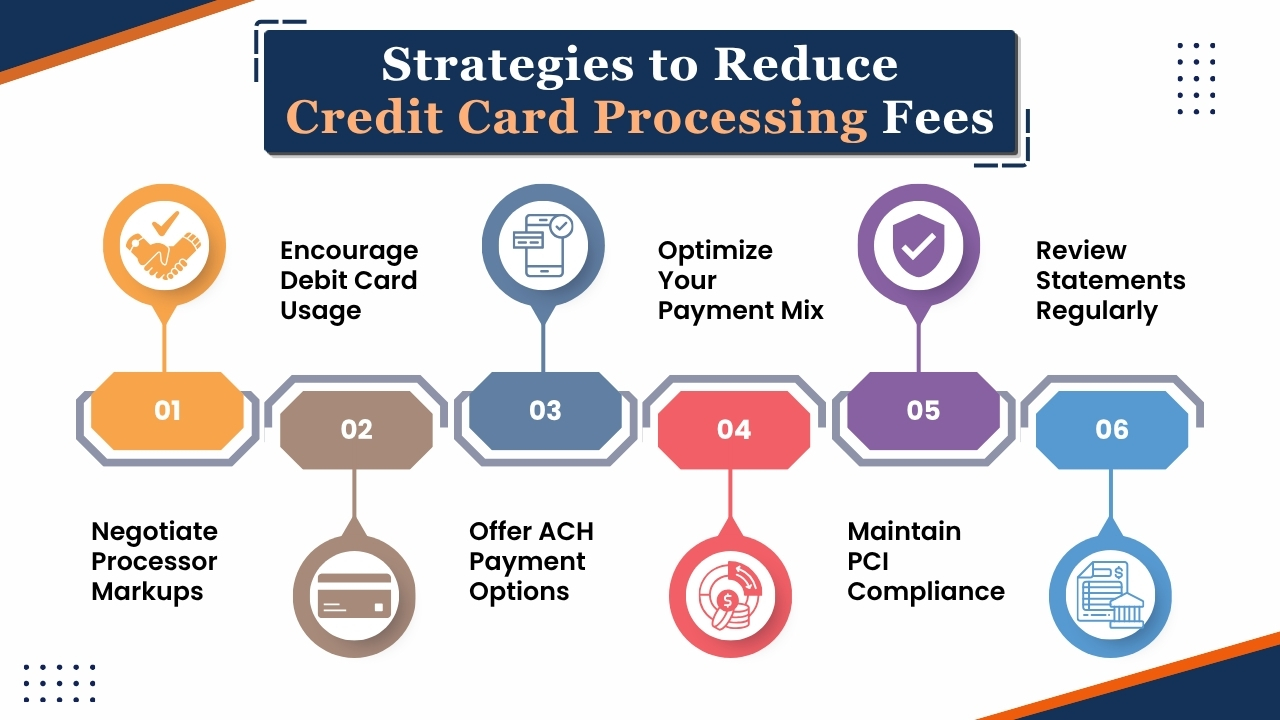

Strategies to Reduce Credit Card Processing Fees

Businesses can take several proactive steps for reducing credit card processing costs without sacrificing convenience of customers.

Implementing the following strategies can help improve profits and reduce unnecessary payment expenses.

1. Negotiate Processor Markups

Many business owners assume processing rates are fixed, but the markup of processors is often negotiable. Established businesses with high sales volume and low chargeback rates may be eligible for better pricing.

While comparing multiple providers and requesting competitive quotes can help merchants to secure lower rates and more favorable contract terms.

2. Encourage Debit Card Usage

Debit card transactions usually have lower interchange fees than credit card transactions. Encouraging customers to use debit cards, mainly for large purchases, helps to reduce overall processing expenses.

Over time, even small savings per transaction can have a high impact on the business.

3. Offer ACH Payment Options

ACH (Automated Clearing House) transfers are less expensive than credit card payments. This payment method is highly beneficial for businesses that process large invoices, recurring payments, or B2B transactions.

Providing ACH as an alternative can highly reduce payment acceptance costs.

4. Optimize Your Payment Mix

Businesses can reduce processing expenses by promoting lower-cost payment methods while still offering customers with multiple payment options.

A balanced payment mix which includes debit cards, ACH transfers, and digital payment solutions can help to reduce overall transaction fees.

5. Maintain PCI Compliance

Meeting Payment Card Industry (PCI) security requirements helps businesses to avoid any expensive penalties due to non-compliance.

Maintaining a secure payment system reduces the risk of data breaches and fraud expenses.

6. Review Statements Regularly

Monthly reviews of merchant statements can reveal billing errors, unnecessary fees, and unexpected rate increases.

While regular audits help businesses to identify saving opportunities and ensure that they are paying only the fees mentioned in the processing agreements.

Conclusion

Credit card processing fees are an effective part of accepting electronic payments. Understanding the crucial components of processing costs such as interchange fees, assessment fees, and processor markups, businesses can have greater transparency into where their money is going and how payment expenses affect overall profits.

Different factors, such as card type, transaction method, industry, and processing volume can highly affect the rates that merchants may pay.

Additionally, selecting the right pricing model such as flat-rate, interchange-plus, tiered, or subscription-based can have a high impact on long-term costs.

Businesses should also pay attention to hidden fees like PCI compliance charges, gateway fees, and chargeback costs that can increase their effective processing rate if left unchecked.

While the good fact is that many processing costs can be managed through strategic actions like negotiating processor markups, encouraging lower-cost payment methods, maintaining PCI compliance, and reviewing merchant statements regularly.

Payment providers like AcePay can also help businesses simplify payment acceptance while offering transparent pricing and modern payment solutions.

Ultimately, understanding and actively managing credit card processing fees helps businesses to reduce costs, improve cash flow, and improve operational efficiency, and make more informed financial decisions which support long-term growth and success.

If you have any query about credit card processing fees then you may book a free demo at AcePay and we are more than happy to assist you.