For businesses and consumers all over the world, credit card processing plays a crucial role in enabling secure and smooth transactions.

Whether customers are shopping online, swipe their cards at retail stores, or use mobile wallets for contactless payments, an advanced payment system works behind the scenes to authorize, verify, and complete every transaction within seconds.

So it is essential for business owners, eCommerce entrepreneurs, and anyone involved in modern digital payment systems to understand how credit card processing works step by step.

The credit card payment process involves several crucial participants which includes the cardholder, merchant, payment gateway, payment processor, acquiring bank, card network, and issuing bank.

Every participant performs a specific function to ensure that payments are processed securely and efficiently.

From the time a customer enters their card details to the final settlement of funds into the merchant’s account, there are many security measures like authentication, encryption, and fraud prevention technologies activated.

Modern payment processing systems can support different payment methods like EMV chip cards, contactless payments, mobile wallets, and online transactions.

Additionally, businesses must understand different concepts like payment authorization, transaction settlement, PCI DSS compliance, credit card processing fees, and chargebacks to manage payments effectively and reduce financial risks.

Through this blog, we will walk you through the complete step-by-step credit card processing workflow, how payment gateways and processors operate, the role of banks and card networks, common transaction fees, security measures, and the latest trends shaping the future of digital payments.

Ultimately, you will have a clear understanding of how money moves securely through the global electronic payment ecosystem.

How Credit Card Processing Works

Credit card processing may look simple for customers. Whenever a customer taps, inserts, swipes, or enters their card details online, within seconds the payment is either approved or declined.

But behind the quick checkout, there are several banks, networks, processors, gateways, security checks, and settlement systems that work together to securely transfer transaction data and funds.

For businesses, understanding how credit card processing works is not just about technology. Instead it directly affects cash flow, customer experience, fraud risk, processing fees, chargebacks, reporting, and the way a business selects its payment provider.

Whether you are running a retail store, restaurant, medical office, online store, service business, nonprofit, subscription platform, or mobile business, the right payment processing setup can help to make checkout faster, reduce payment issues, and helps to control expenses.

A credit card processing system enables businesses to accept card payments through a point-of-sale system, payment terminal, mobile reader, online checkout, invoice, payment link or virtual terminal.

The payment flow involves securely transmitting transaction information across the customer, merchant, payment processor, card network, the issuing bank, and acquiring bank to complete the transaction.

In most transactions, while authorization is usually completed within seconds, the settlement and funding stages may take longer based on the payment provider, bank processing timelines, risk checks, and batch settlement cycles.

Credit card processing is a multi-step system that securely transmits payment data and transfers funds through authorization, clearing, and settlement stages involving the customer, merchant, financial, institutions, and card networks.

Key Parties Involved in Credit Card Processing

A credit card transaction involves several participants. Every participant has a specific role in approving the payment, moving information, calculating fees, and transferring funds.

The cardholder is the customer using a credit card, debit card, or digital wallet to pay for goods or services. The merchant is the business accepting the payment.

The merchant may accept payments through a store terminal, website checkout, POS system, mobile app, or virtual terminal.

The issuing bank is the customer’s bank or financial institution. This bank issued the card to the customer and decided whether the transaction should be approved or declined.

The issuer checks whether the account is active, whether enough credit or funds are available, and whether fraud signals are present.

The acquiring bank, also called the merchant bank, works on the merchant side. It receives transaction funds and helps deposit them into the merchant account or business bank account.

The card networks, like Visa, Mastercard, American Express, and Discover, connect issuing banks and acquiring banks. They set rules, standards, and assessment fees and help route transaction data.

The payment processor manages the flow of transaction information between the merchant, banks, and card networks. This helps to authorize, process, settle, and report transactions.

The payment gateway is especially crucial for online payments. It encrypts and securely sends payment data from a website, app, payment page, or ecommerce platform to the processor. For in-person sales, the POS system or terminal captures the card information and sends the transaction request.

Credit card processing involves several important participants, including the cardholder, merchant, payment processor, issuing bank, acquiring bank, card network, payment gateway, and POS system, all working together to securely authorize and complete electronic transactions.

The Three Main Stages of Credit Card Processing

Credit card processing can be understood in three main stages: authorization, settlement, and funding. Although some payment systems distinguish clearing and settlement as separate stages, the overall process follows the same flow: the transaction is first authorized, then processed and finalized between financial institutions, and finally the funds are transferred to the merchant’s account.

1. Authorization

Authorization is the first stage. It begins when the customer presents their card or enters their payment details. In a store, this may happen through a card terminal, POS system, or contactless reader. While online, it happens through a checkout page, payment form, or payment gateway.

The merchant’s system sends the payment request to the processor. The processor routes the request through the card network to the issuing bank.

The issuing bank checks the cardholder’s account, available funds or credit, card status, expiration date, fraud indicators, and sometimes security details like CVV and address verification. Then the issuer approves or declines the transaction.

If the transaction is approved, an authorization code is sent back through the same chain to the merchant’s system. The customer sees an approved payment, and the business can complete the sale. If the transaction is declined, the sales does not go through unless the customer uses another payment method.

Authorization usually happens in seconds. During authorization, the payment request moves from the merchant through the payment processor and card network to the issuing bank, which then sends an approval or decline response back through the payment processor and card network to the issuing bank, which sends an approval or decline response back through the same channel to complete the transaction decision.

2. Clearing and Settlement

Authorization does not indicate that the merchant has already received the money. Rather it only means the customer’s bank has approved the transaction. While settlement is the stage where approved transactions are submitted for payment.

At the end of each day, many merchants group approved transactions into a batch and submit them together for final processing and settlement. The merchant submits a batch of authorized transactions to the processor.

The processor sends the details to the acquiring bank and card networks. The card networks coordinate with issuing banks to calculate fees, confirm transaction records, and move the funds.

During this stage, the issuer charges the cardholder’s account, and funds are routed toward the acquiring bank. Various costs, including interchange fees, assessment fees, and processor markups, are applied and deducted based on the merchant’s selected pricing model.

Settlement is the stage in which approved transactions are submitted for processing, and card networks work with issuing banks to move funds through the system and deposit them into the acquiring bank before reaching the merchant’s account.

3. Funding

Funding is when the merchant receives the money. After settlement is completed, the acquiring bank or processor deposits the funds into the merchant account or business bank account after deducting the relevant processing fees.

Funding timelines can differ by provider, with some offering same-day or next-day deposits, while others may require a few additional business days to complete the transfer.

The exact timing of fund deposits may differ based on factors like daily processing cut-off schedules, weekends, and bank holidays, the payment processor’s policies, risk assessments, the type of industry, and the merchant’s business history or account age.

Many small businesses usually receive card payment funds within one to five business days, based on the payment processor’s funding schedule and other operational factors.

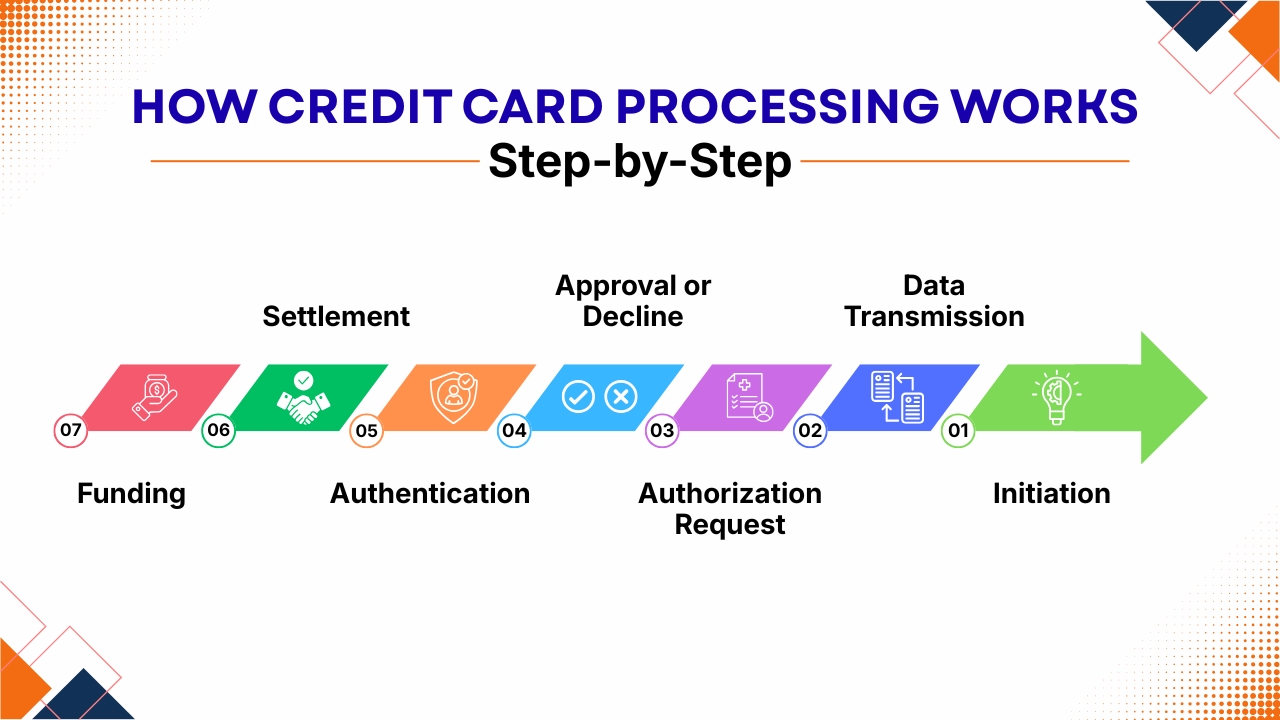

How Credit Card Processing Works Step-by-Step

1. Initiation

The credit card processing begins when a customer makes a purchase online, in-store, or through a mobile app. The customer enters, taps, swipes, or inserts their card details into a payment system or gateway.

This system securely encrypts the card information to protect sensitive financial data before sending it for further processing.

2. Data Transmission

After encryption, the payment information is transmitted to the payment processor. The processor then works as an intermediary between merchants, banks, and card networks.

It identifies the card type like Visa or Mastercard, and forwards the transaction details through the accurate financial network securely and quickly.

3. Authorization Request

The card network sends the transaction request to the issuing bank, which is also the customer’s bank. Then the bank checks whether the card is valid, whether there is enough balance or credit available, and whether the transaction seems suspicious or fraudulent before making a decision.

4. Approval or Decline

The issuing bank responds whether the transaction is approved or declined, If the transaction is approved, then the purchase amount is on a temporary basis reserved in the customer’s account.

If the transaction is declined, the transaction is cancelled immediately, and the merchant is informed about the failed payment.

5. Authentication

Authentication verified the identity of the cardholder. Through security measures like OTPs, CVV verification, and fraud detection systems ensure that the transaction complies with banking regulations and remains secure from unauthorized access or misuse.

6. Settlement

At the end of the day, the merchant sends approved transactions for settlement. The processor coordinates with banks and card networks to transfer funds from the customer’s account to the merchant’s acquiring bank securely and efficiently.

7. Funding

Finally, the acquiring bank deposits the settled funds into the merchant’s business account. This process generally takes one to three business days, depending on the processor, bank policies, and transaction type.

Step-by-Step Example of a Credit Card Transaction

Imagine a customer buying a $100 product from a retail store. First, the customer taps their card at the payment terminal. The terminal captures the payment information and sends the transaction request to the payment processor. The processor forwards the data through the correct card network to the customer’s issuing bank.

The issuing bank checks the account. It confirms that the card is valid, the customer has available credit or funds, and the transaction does not appear suspicious. The bank approves the payment and sends an authorization response back through the card network and processor to the merchant’s terminal.

After the payment is approved, the customer completes the purchase and takes the product, while the actual transfer of funds to the merchant’s account is finalized later during the settlement process.

At the end of the day, the merchant groups all authorized transactions together and submits them for settlement processing. The processor sends those transactions for settlement.

The issuing bank transfers funds through the card network to the acquiring bank, deducting interchange and network fees. The processor and merchant services provider may also deduct their markup or service fees.

Finally, the net amount is deposited into the business bank account. The merchant may see the deposit the next day, in two or three days, or later based on the provider’s schedule and risk controls.

Credit Card Processing Fees Explained

Credit card processing fees are the costs businesses pay to accept electronic payments from customers. These fees cover the services provided by banks, card networks, payment processors, gateways, and fraud prevention systems which help to authorize, secure, and complete every transaction.

The total processing cost can differ based on factors like transaction type, payment method, business industry, risk level, monthly sales volume, and the provider’s pricing structure. Understanding these fees helps businesses to manage expenses and choose the right payment processing solution.

1. Interchange Fees

Interchange fees are usually the largest percentage of credit card processing costs. These fees are paid to the issuing bank that provided the customer’s card.

While the amount of fees depends on several factors including whether the transaction is card-present or card-not-present, the type of card used, and the overall fraud risk.

For instance, in-store chip transactions usually have lower fees than manually entered online payments as they are considered more secure. Reward cards and premium credit cards may also carry higher interchange rates than standard debit cards.

2. Assessment Fees

Assessment fees are charged by card networks like Visa, Mastercard, and other payment brands. These fees help to maintain the payment infrastructure, transaction routing systems, and operational networks which allow electronic payments to function smoothly.

Although assessment fees are usually smaller than interchange fees, they are applied to every transaction processed through the network.

3. Processor Markup Fees

Payment processors and merchant service providers charge markup fees for handling transactions and providing payment services. Such costs may appear as a percentage fee, flat transaction fee, monthly account fee, or gateway charge.

Unlike interchange and assessment fees, processor markups can often be negotiated depending on the business size, sales volume, and pricing model selected by the merchant.

4. Gateway, Equipment, and Software Fees

Businesses may also pay additional fees for payment gateways, POS systems, card readers, terminals, and software subscriptions. Online businesses commonly pay gateway fees for secure payment processing, while retail businesses may invest in payment hardware.

Some providers offer equipment purchases, while other providers provide leasing options that may become more expensive over time.

5. Chargeback and Dispute Fees

Chargeback fees occur when customers dispute transactions with their card issuer. Additionally to losing the sale amount temporarily, merchants may pay dispute handling fees and spend time responding to the claim.

Excessive chargebacks can increase processing costs, trigger payment holds, or even lead to account termination by the processor.

Common Credit Card Processing Pricing Models

Before selecting a payment provider it is essential to understand credit card processing pricing models. As different processors have different fee structures, the lowest advertised rate may not always result in the lowest overall cost.

Businesses should also compare pricing transparency, transaction fees, monthly charges, and additional service costs carefully. The ideal pricing model depends on factors like monthly charges, and additional service costs carefully.

The ideal pricing model depends on factors such as monthly sales volume, average transaction value, online or in-store payment methods, industry risk level, and whether the business prefers flexible rates or predictable monthly billing.

1. Flat-Rate Pricing

Flat-rate pricing charges a fixed percentage, often with a fixed transaction fee. It is simple, predictable, and popular with startups and smaller businesses. The downside is that it may cost more as volume grows because lower-cost card types are bundled into the same general rate.

2. Interchange-Plus Pricing

Interchange-plus pricing separates the actual interchange cost from the processor’s markup. This model is usually more transparent because you can see what goes to banks and networks versus what goes to your processor. It can be cost-effective for established businesses with higher processing volume.

3. Tiered Pricing

Tiered pricing organizes transactions into different categories like qualified, mid-qualified, and non-qualified which can make costs less transparent as merchants may not always know why a transaction is placed in a higher-category fee category which causes many businesses to choose simpler and more transparent pricing structures.

4. Subscription Pricing

Subscription pricing charges a monthly membership fee plus a lower per-transaction markup. It may work well for businesses with high volume or larger average ticket sizes, but it may not be ideal for low-volume businesses.

These pricing models and notes that businesses commonly evaluate interchange-plus, flat-rate, subscription, and tiered structures.

Online vs In-Person Credit Card Processing

Online and in-person credit card payments have the same basic payment flow which includes authorization, processing, settlement, and funding. But the technology, security methods, and fraud risks involved with both online and in-person credit card processing are quite different.

In-person transactions usually happen through POS terminals, chip readers, contactless devices, or mobile wallets, where the customer physically presents the card or payment device.

These transactions are usually more secure as it uses EMV chip technology and tokenized mobile wallet payments and tokenized mobile wallet use encrypted and dynamic transaction data.

On the contrary, online payments are categorized as card-not-present transactions as the merchants cannot physically verify the card. Due to which online businesses face higher fraud and chargeback risks.

For improving security, merchants use payment gateways, encrypted checkout pages, CVV verification, address verification systems, fraud detection tools and tokenization technologies.

For omnichannel businesses, integrating online, mobile, recurring, invoice, and in-store payments into a single centralized system helps to simplify reporting, customer management, refund tracking, handling disputes, and overall payment monitoring across all sales channels.

Conclusion

Credit card processing is a complex system and also highly efficient systems that enables businesses to accept secure electronic payments both online and in physical stores.

Though the payment transaction seems to be done instantly to customers but behind the scenes there are several crucial steps taking place that include authorization, authentication, clearing, settlement, and funding.

Multiple components such as cardholder, merchant, payment processor, issuing bank, acquiring bank, card network, and payment gateway work together for completing every transaction safely and accurately.

Understanding how credit card processing works step by step helps businesses make smarter decisions about payment systems, pricing models, fraud prevention, and customer experience.

This helps merchants to understand why processing fees exist, how settlement timelines work, and know what factors influence funding speed and transaction costs.

While digital payments continue to evolve, businesses are adopting advanced payment technologies like contactless payments, mobile wallets, tokenization, AI-based fraud detection, and real-time payment processing. Customers now expect fast, seamless, and secure payment experiences across every channel.

Selecting the right payment processor and understanding the complete payment lifecycle can improve operational efficiency, reduce payment concerns, and support long-term business growth.

Whether you are running a retail store, eCommerce website, subscription business, or service company, having a clear understanding of credit card processing is essential in today’s modern economy.

If you still have any query about how credit card processing works step by step then you may book a free demo at AcePay and we are more than happy to assist you.