For businesses and consumers all over the world, credit card processing plays a crucial role in enabling secure and smooth transactions.

Whether customers are shopping online, swipe their cards at retail stores, or use mobile wallets for contactless payments, an advanced payment system works behind the scenes to authorize, verify, and complete every transaction within seconds.

So it is essential for business owners, eCommerce entrepreneurs, and anyone involved in modern digital payment systems to understand how credit card processing works step by step.

The credit card payment process involves several crucial participants which includes the cardholder, merchant, payment gateway, payment processor, acquiring bank, card network, and issuing bank.

Every participant performs a specific function to ensure that payments are processed securely and efficiently.

From the time a customer enters their card details to the final settlement of funds into the merchant’s account, there are many security measures like authentication, encryption, and fraud prevention technologies activated.

Modern payment processing systems can support different payment methods like EMV chip cards, contactless payments, mobile wallets, and online transactions.

Additionally, businesses must understand different concepts like payment authorization, transaction settlement, PCI DSS compliance, credit card processing fees, and chargebacks to manage payments effectively and reduce financial risks.

Through this blog, we will walk you through the complete step-by-step credit card processing workflow, how payment gateways and processors operate, the role of banks and card networks, common transaction fees, security measures, and the latest trends shaping the future of digital payments.

Ultimately, you will have a clear understanding of how money moves securely through the global electronic payment ecosystem.

How Credit Card Processing Works

Credit card processing may look simple for customers. Whenever a customer taps, inserts, swipes, or enters their card details online, within seconds the payment is either approved or declined.

But behind the quick checkout, there are several banks, networks, processors, gateways, security checks, and settlement systems that work together to securely transfer transaction data and funds.

For businesses, understanding how credit card processing works is not just about technology. Instead it directly affects cash flow, customer experience, fraud risk, processing fees, chargebacks, reporting, and the way a business selects its payment provider.

Whether you are running a retail store, restaurant, medical office, online store, service business, nonprofit, subscription platform, or mobile business, the right payment processing setup can help to make checkout faster, reduce payment issues, and helps to control expenses.

A credit card processing system enables businesses to accept card payments through a point-of-sale system, payment terminal, mobile reader, online checkout, invoice, payment link or virtual terminal.

The payment flow involves securely transmitting transaction information across the customer, merchant, payment processor, card network, the issuing bank, and acquiring bank to complete the transaction.

In most transactions, while authorization is usually completed within seconds, the settlement and funding stages may take longer based on the payment provider, bank processing timelines, risk checks, and batch settlement cycles.

Credit card processing is a multi-step system that securely transmits payment data and transfers funds through authorization, clearing, and settlement stages involving the customer, merchant, financial, institutions, and card networks.

Key Parties Involved in Credit Card Processing

A credit card transaction involves several participants. Every participant has a specific role in approving the payment, moving information, calculating fees, and transferring funds.

The cardholder is the customer using a credit card, debit card, or digital wallet to pay for goods or services. The merchant is the business accepting the payment.

The merchant may accept payments through a store terminal, website checkout, POS system, mobile app, or virtual terminal.

The issuing bank is the customer’s bank or financial institution. This bank issued the card to the customer and decided whether the transaction should be approved or declined.

The issuer checks whether the account is active, whether enough credit or funds are available, and whether fraud signals are present.

The acquiring bank, also called the merchant bank, works on the merchant side. It receives transaction funds and helps deposit them into the merchant account or business bank account.

The card networks, like Visa, Mastercard, American Express, and Discover, connect issuing banks and acquiring banks. They set rules, standards, and assessment fees and help route transaction data.

The payment processor manages the flow of transaction information between the merchant, banks, and card networks. This helps to authorize, process, settle, and report transactions.

The payment gateway is especially crucial for online payments. It encrypts and securely sends payment data from a website, app, payment page, or ecommerce platform to the processor. For in-person sales, the POS system or terminal captures the card information and sends the transaction request.

Credit card processing involves several important participants, including the cardholder, merchant, payment processor, issuing bank, acquiring bank, card network, payment gateway, and POS system, all working together to securely authorize and complete electronic transactions.

The Three Main Stages of Credit Card Processing

Credit card processing can be understood in three main stages: authorization, settlement, and funding. Although some payment systems distinguish clearing and settlement as separate stages, the overall process follows the same flow: the transaction is first authorized, then processed and finalized between financial institutions, and finally the funds are transferred to the merchant’s account.

1. Authorization

Authorization is the first stage. It begins when the customer presents their card or enters their payment details. In a store, this may happen through a card terminal, POS system, or contactless reader. While online, it happens through a checkout page, payment form, or payment gateway.

The merchant’s system sends the payment request to the processor. The processor routes the request through the card network to the issuing bank.

The issuing bank checks the cardholder’s account, available funds or credit, card status, expiration date, fraud indicators, and sometimes security details like CVV and address verification. Then the issuer approves or declines the transaction.

If the transaction is approved, an authorization code is sent back through the same chain to the merchant’s system. The customer sees an approved payment, and the business can complete the sale. If the transaction is declined, the sales does not go through unless the customer uses another payment method.

Authorization usually happens in seconds. During authorization, the payment request moves from the merchant through the payment processor and card network to the issuing bank, which then sends an approval or decline response back through the payment processor and card network to the issuing bank, which sends an approval or decline response back through the same channel to complete the transaction decision.

2. Clearing and Settlement

Authorization does not indicate that the merchant has already received the money. Rather it only means the customer’s bank has approved the transaction. While settlement is the stage where approved transactions are submitted for payment.

At the end of each day, many merchants group approved transactions into a batch and submit them together for final processing and settlement. The merchant submits a batch of authorized transactions to the processor.

The processor sends the details to the acquiring bank and card networks. The card networks coordinate with issuing banks to calculate fees, confirm transaction records, and move the funds.

During this stage, the issuer charges the cardholder’s account, and funds are routed toward the acquiring bank. Various costs, including interchange fees, assessment fees, and processor markups, are applied and deducted based on the merchant’s selected pricing model.

Settlement is the stage in which approved transactions are submitted for processing, and card networks work with issuing banks to move funds through the system and deposit them into the acquiring bank before reaching the merchant’s account.

3. Funding

Funding is when the merchant receives the money. After settlement is completed, the acquiring bank or processor deposits the funds into the merchant account or business bank account after deducting the relevant processing fees.

Funding timelines can differ by provider, with some offering same-day or next-day deposits, while others may require a few additional business days to complete the transfer.

The exact timing of fund deposits may differ based on factors like daily processing cut-off schedules, weekends, and bank holidays, the payment processor’s policies, risk assessments, the type of industry, and the merchant’s business history or account age.

Many small businesses usually receive card payment funds within one to five business days, based on the payment processor’s funding schedule and other operational factors.

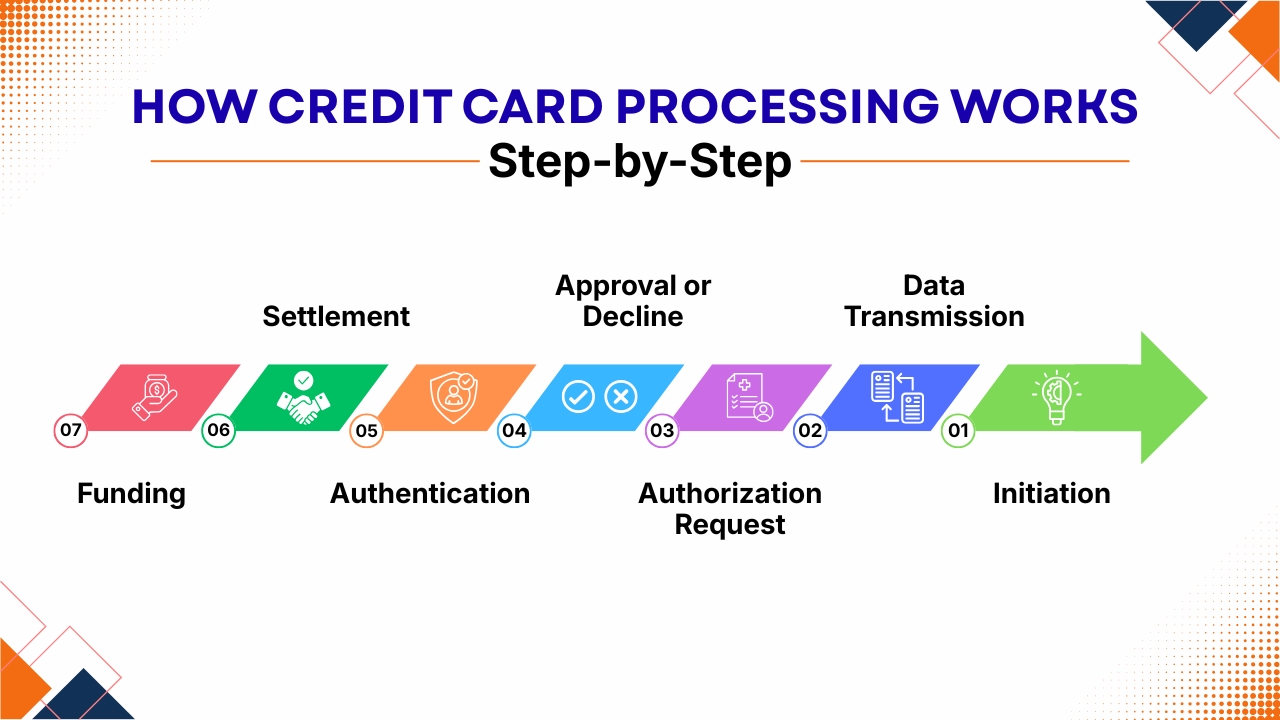

How Credit Card Processing Works Step-by-Step

1. Initiation

The credit card processing begins when a customer makes a purchase online, in-store, or through a mobile app. The customer enters, taps, swipes, or inserts their card details into a payment system or gateway.

This system securely encrypts the card information to protect sensitive financial data before sending it for further processing.

2. Data Transmission

After encryption, the payment information is transmitted to the payment processor. The processor then works as an intermediary between merchants, banks, and card networks.

It identifies the card type like Visa or Mastercard, and forwards the transaction details through the accurate financial network securely and quickly.

3. Authorization Request

The card network sends the transaction request to the issuing bank, which is also the customer’s bank. Then the bank checks whether the card is valid, whether there is enough balance or credit available, and whether the transaction seems suspicious or fraudulent before making a decision.

4. Approval or Decline

The issuing bank responds whether the transaction is approved or declined, If the transaction is approved, then the purchase amount is on a temporary basis reserved in the customer’s account.

If the transaction is declined, the transaction is cancelled immediately, and the merchant is informed about the failed payment.

5. Authentication

Authentication verified the identity of the cardholder. Through security measures like OTPs, CVV verification, and fraud detection systems ensure that the transaction complies with banking regulations and remains secure from unauthorized access or misuse.

6. Settlement

At the end of the day, the merchant sends approved transactions for settlement. The processor coordinates with banks and card networks to transfer funds from the customer’s account to the merchant’s acquiring bank securely and efficiently.

7. Funding

Finally, the acquiring bank deposits the settled funds into the merchant’s business account. This process generally takes one to three business days, depending on the processor, bank policies, and transaction type.

Step-by-Step Example of a Credit Card Transaction

Imagine a customer buying a $100 product from a retail store. First, the customer taps their card at the payment terminal. The terminal captures the payment information and sends the transaction request to the payment processor. The processor forwards the data through the correct card network to the customer’s issuing bank.

The issuing bank checks the account. It confirms that the card is valid, the customer has available credit or funds, and the transaction does not appear suspicious. The bank approves the payment and sends an authorization response back through the card network and processor to the merchant’s terminal.

After the payment is approved, the customer completes the purchase and takes the product, while the actual transfer of funds to the merchant’s account is finalized later during the settlement process.

At the end of the day, the merchant groups all authorized transactions together and submits them for settlement processing. The processor sends those transactions for settlement.

The issuing bank transfers funds through the card network to the acquiring bank, deducting interchange and network fees. The processor and merchant services provider may also deduct their markup or service fees.

Finally, the net amount is deposited into the business bank account. The merchant may see the deposit the next day, in two or three days, or later based on the provider’s schedule and risk controls.

Credit Card Processing Fees Explained

Credit card processing fees are the costs businesses pay to accept electronic payments from customers. These fees cover the services provided by banks, card networks, payment processors, gateways, and fraud prevention systems which help to authorize, secure, and complete every transaction.

The total processing cost can differ based on factors like transaction type, payment method, business industry, risk level, monthly sales volume, and the provider’s pricing structure. Understanding these fees helps businesses to manage expenses and choose the right payment processing solution.

1. Interchange Fees

Interchange fees are usually the largest percentage of credit card processing costs. These fees are paid to the issuing bank that provided the customer’s card.

While the amount of fees depends on several factors including whether the transaction is card-present or card-not-present, the type of card used, and the overall fraud risk.

For instance, in-store chip transactions usually have lower fees than manually entered online payments as they are considered more secure. Reward cards and premium credit cards may also carry higher interchange rates than standard debit cards.

2. Assessment Fees

Assessment fees are charged by card networks like Visa, Mastercard, and other payment brands. These fees help to maintain the payment infrastructure, transaction routing systems, and operational networks which allow electronic payments to function smoothly.

Although assessment fees are usually smaller than interchange fees, they are applied to every transaction processed through the network.

3. Processor Markup Fees

Payment processors and merchant service providers charge markup fees for handling transactions and providing payment services. Such costs may appear as a percentage fee, flat transaction fee, monthly account fee, or gateway charge.

Unlike interchange and assessment fees, processor markups can often be negotiated depending on the business size, sales volume, and pricing model selected by the merchant.

4. Gateway, Equipment, and Software Fees

Businesses may also pay additional fees for payment gateways, POS systems, card readers, terminals, and software subscriptions. Online businesses commonly pay gateway fees for secure payment processing, while retail businesses may invest in payment hardware.

Some providers offer equipment purchases, while other providers provide leasing options that may become more expensive over time.

5. Chargeback and Dispute Fees

Chargeback fees occur when customers dispute transactions with their card issuer. Additionally to losing the sale amount temporarily, merchants may pay dispute handling fees and spend time responding to the claim.

Excessive chargebacks can increase processing costs, trigger payment holds, or even lead to account termination by the processor.

Common Credit Card Processing Pricing Models

Before selecting a payment provider it is essential to understand credit card processing pricing models. As different processors have different fee structures, the lowest advertised rate may not always result in the lowest overall cost.

Businesses should also compare pricing transparency, transaction fees, monthly charges, and additional service costs carefully. The ideal pricing model depends on factors like monthly charges, and additional service costs carefully.

The ideal pricing model depends on factors such as monthly sales volume, average transaction value, online or in-store payment methods, industry risk level, and whether the business prefers flexible rates or predictable monthly billing.

1. Flat-Rate Pricing

Flat-rate pricing charges a fixed percentage, often with a fixed transaction fee. It is simple, predictable, and popular with startups and smaller businesses. The downside is that it may cost more as volume grows because lower-cost card types are bundled into the same general rate.

2. Interchange-Plus Pricing

Interchange-plus pricing separates the actual interchange cost from the processor’s markup. This model is usually more transparent because you can see what goes to banks and networks versus what goes to your processor. It can be cost-effective for established businesses with higher processing volume.

3. Tiered Pricing

Tiered pricing organizes transactions into different categories like qualified, mid-qualified, and non-qualified which can make costs less transparent as merchants may not always know why a transaction is placed in a higher-category fee category which causes many businesses to choose simpler and more transparent pricing structures.

4. Subscription Pricing

Subscription pricing charges a monthly membership fee plus a lower per-transaction markup. It may work well for businesses with high volume or larger average ticket sizes, but it may not be ideal for low-volume businesses.

These pricing models and notes that businesses commonly evaluate interchange-plus, flat-rate, subscription, and tiered structures.

Online vs In-Person Credit Card Processing

Online and in-person credit card payments have the same basic payment flow which includes authorization, processing, settlement, and funding. But the technology, security methods, and fraud risks involved with both online and in-person credit card processing are quite different.

In-person transactions usually happen through POS terminals, chip readers, contactless devices, or mobile wallets, where the customer physically presents the card or payment device.

These transactions are usually more secure as it uses EMV chip technology and tokenized mobile wallet payments and tokenized mobile wallet use encrypted and dynamic transaction data.

On the contrary, online payments are categorized as card-not-present transactions as the merchants cannot physically verify the card. Due to which online businesses face higher fraud and chargeback risks.

For improving security, merchants use payment gateways, encrypted checkout pages, CVV verification, address verification systems, fraud detection tools and tokenization technologies.

For omnichannel businesses, integrating online, mobile, recurring, invoice, and in-store payments into a single centralized system helps to simplify reporting, customer management, refund tracking, handling disputes, and overall payment monitoring across all sales channels.

Conclusion

Credit card processing is a complex system and also highly efficient systems that enables businesses to accept secure electronic payments both online and in physical stores.

Though the payment transaction seems to be done instantly to customers but behind the scenes there are several crucial steps taking place that include authorization, authentication, clearing, settlement, and funding.

Multiple components such as cardholder, merchant, payment processor, issuing bank, acquiring bank, card network, and payment gateway work together for completing every transaction safely and accurately.

Understanding how credit card processing works step by step helps businesses make smarter decisions about payment systems, pricing models, fraud prevention, and customer experience.

This helps merchants to understand why processing fees exist, how settlement timelines work, and know what factors influence funding speed and transaction costs.

While digital payments continue to evolve, businesses are adopting advanced payment technologies like contactless payments, mobile wallets, tokenization, AI-based fraud detection, and real-time payment processing. Customers now expect fast, seamless, and secure payment experiences across every channel.

Selecting the right payment processor and understanding the complete payment lifecycle can improve operational efficiency, reduce payment concerns, and support long-term business growth.

Whether you are running a retail store, eCommerce website, subscription business, or service company, having a clear understanding of credit card processing is essential in today’s modern economy.

If you still have any query about how credit card processing works step by step then you may book a free demo at AcePay and we are more than happy to assist you.

In a quickly changing digital economy, businesses operating in industries that have high fraud risks, chargeback ratios, or complex regulatory requirements usually face difficulty to secure reliable payment services. And this is where Payment Processing solutions for High-Risk businesses become essential.

Unlike standard merchant accounts, high-risk payment processing specifically supports businesses that traditional banks and payment providers may feel risky to support due to industry type, transaction volume, recurring billing models, or international operations.

Many industries like online gaming, travel, CBD, cryptocurrency, subscription services, and nutraceuticals often require specialized high-risk merchant accounts for accepting payments smoothly without any interruptions.

Without the right processing partner high-risk businesses may face many issues like account freezes, delayed settlements, rolling reserves, or even termination of services.

Hence it is crucial for high risk businesses to select the accurate high-risk payment gateway for long-term stability and business growth.

Modern payment processing solutions offer advanced fraud prevention tools, chargeback management systems, multi-currency payment support, and secure transaction technologies that help businesses to minimize financial risks and also improve customer experience.

Additionally, many providers offer scalable systems, support alternative payment methods, and global acquiring solutions that support online businesses.

While eCommerce keeps growing all over the world, the demand for reliable payment solutions for high-risk businesses is increasing.

Today companies require payment systems which not just process transactions efficiently but also give compliance support, advanced security, and flexible underwriting.

Businesses by understanding how high-risk payment processors work and selecting the right provider may help businesses to improve approval rates, reduce disputes, and achieve revenue growth in a highly competitive market.

What Makes a Business High Risk?

Businesses can be categorized as high risk due to many factors such as high chargeback rates, recurring billing models, high transaction volumes, international sales, or operating in industries that have strict regulatory inspections.

For instance, online gambling, CBD, nutraceuticals, travel, ticketing, tobacco, and subscription businesses are frequently reviewed more carefully because they tend to generate more disputes, refund requests, legal requirements, or compliance concerns.

In other cases, the risk is due to the transaction model. Card-not-present payments, online orders, phone payments, international transactions, multiple currencies, high average order values, recurring billing, free trials, delayed delivery, and digital products can all increase financial and fraud-related risks for payment processors.

Businesses that handle international transactions, process multiple currencies, offer subscription-based services, sell intangible products, manage high-value transactions, or have a history of terminated merchant accounts which are often categorized as high-risk by payment processors.

Payment processors also evaluate a merchant’s business history, and also factors like poor credit records, frequent customer disputes, excessive refunds, lack of prior processing experience, terminated accounts, unclear business policies, or incomplete documentation can result in a high-risk classification.

But the important point is that being classified as high risk is not necessarily negative; rather it is simply a risk assessment category used by payment processors to verify potential financial exposure, determine processing fees, set reserve requirements, and establish the security measures needed before approving a merchant account.

High-Risk Merchant Account vs Payment Gateway

Many merchants confuse payment gateways with a merchant account that are identical, but in reality they serve different roles within the payment processing system.

A payment gateway acts as the secure technology interface that collects customer payment information, encrypts sensitive data, transmits authorization requests, and connects your website, app, invoice, virtual terminal, or POS system to the payment network. It does not usually hold your funds.

A merchant account is the financial account where card payment funds are temporarily before settlement to your business bank account. The acquiring bank or processor reviews your business, accepts the risk, and sets account terms like pricing, reserves, settlement timing, processing limits, and chargeback controls.

The main difference between the two is that the payment gateway securely processes and transmits transaction data, while the merchant account works as the holding account where funds that are approved are temporarily stored before it is transferred to the merchant’s business bank account.

For high-risk businesses, both payment gateway and merchant account are equally crucial roles as a business may still face operational disruptions and financial risks when the gateway does not have advanced fraud protection, intelligent routing, recurring billing functionality, flexible tokenization, detailed reporting, or support for alternative payment methods, even after securing account approval.

A strong payment gateway with a poor merchant account can also fail if fees are too high, reserves are excessive, settlement is slow, or underwriting does not match your business model.

The best setup combines both a high-risk friendly merchant account and a gateway built for fraud control, customer experience, reporting, and scalability.

Why High-Risk Businesses Need Specialized Payment Processing

High-risk merchants need specialized payment processing solutions because traditional providers only support low-risk businesses with predictable transaction patterns, minimal chargebacks, clear delivery timelines, and low compliance complexity.

A specialized high-risk processor understands to verify businesses that other providers reject. Rather than instantly rejecting an application because of the category, they review the complete picture about business model, ownership, website, refund policy, fulfillment process, compliance documents, processing volume, chargeback history, fraud controls, and financial stability.

High-risk processors may also offer tools that standard providers do not prioritize such as rolling reserve management, chargeback alerts, fraud scoring, blacklist controls, multi-currency support, recurring billing management, industry-specific underwriting.

They also provide advanced features like dynamic transaction routing, access to multiple merchant IDs, local acquiring options, real-time reporting, fraud prevention systems, chargeback monitoring, tokenization, and compliance management tools to improve approval rates and reduce financial risk.

For merchants, it matters because payment stability is business stability. If your account is frozen, terminated, or placed under high reserve, revenue can stop almost instantly. A specialized solution reduces that risk by implementing preventive risk controls that identify and address potential issues early, before they turn into serious operational or financial disruptions.

Common Challenges High-Risk Merchants Face

The first challenge high-risk merchants face is approval. High-risk applications usually need more documentation than standard accounts.

Processors may ask for business registration documents, ownership details, bank statements, processing history, chargeback reports, supplier invoices, refund policies, fulfillment details, product descriptions, compliance licenses, website screenshots, marketing material, and customer service procedures.

The second challenge is cost. High-risk businesses often pay higher transaction fees because the processor is accepting more liability. Because high-risk merchants may face higher processing fees, cash reserves, higher chargeback fees, and longer application processes.

High-risk pricing may include higher transaction fees, rolling reserves, separate chargeback fees, and administrative costs connected to compliance requirements.

The third challenge is reserves. A rolling reserve means the processor will hold a percentage of each transaction for a period of time to protect against chargebacks or losses. For instance, a processor may hold 5% to 10% of processed volume for 90 to 180 days. Some merchants may also face fixed reserves, capped reserves, or delayed settlements.

The fourth challenge is chargebacks. High-risk businesses are monitored closely because excessive chargebacks can damage the processor’s credibility with acquiring banks and card networks, ultimately affecting their ability to maintain stable payment processing relationships.

High-risk merchants must continuously track chargeback ratios and ensure compliance with payment network rules, as excessive dispute activity can place their merchant account(MID) at risk of penalties, processing holds, or account termination.

The fifth challenge is account continuity. Relying on only one merchant account creates a significant vulnerability, as any disruption, suspension, or termination can immediately stop a business’s ability to process payments and generate revenue.

If the account is closed or funds are held, the businesses may lose their ability to accept payments. This is why larger or more complex high-risk businesses often require backup processing options, multiple MIDs, or a gateway setup that allows easier migration.

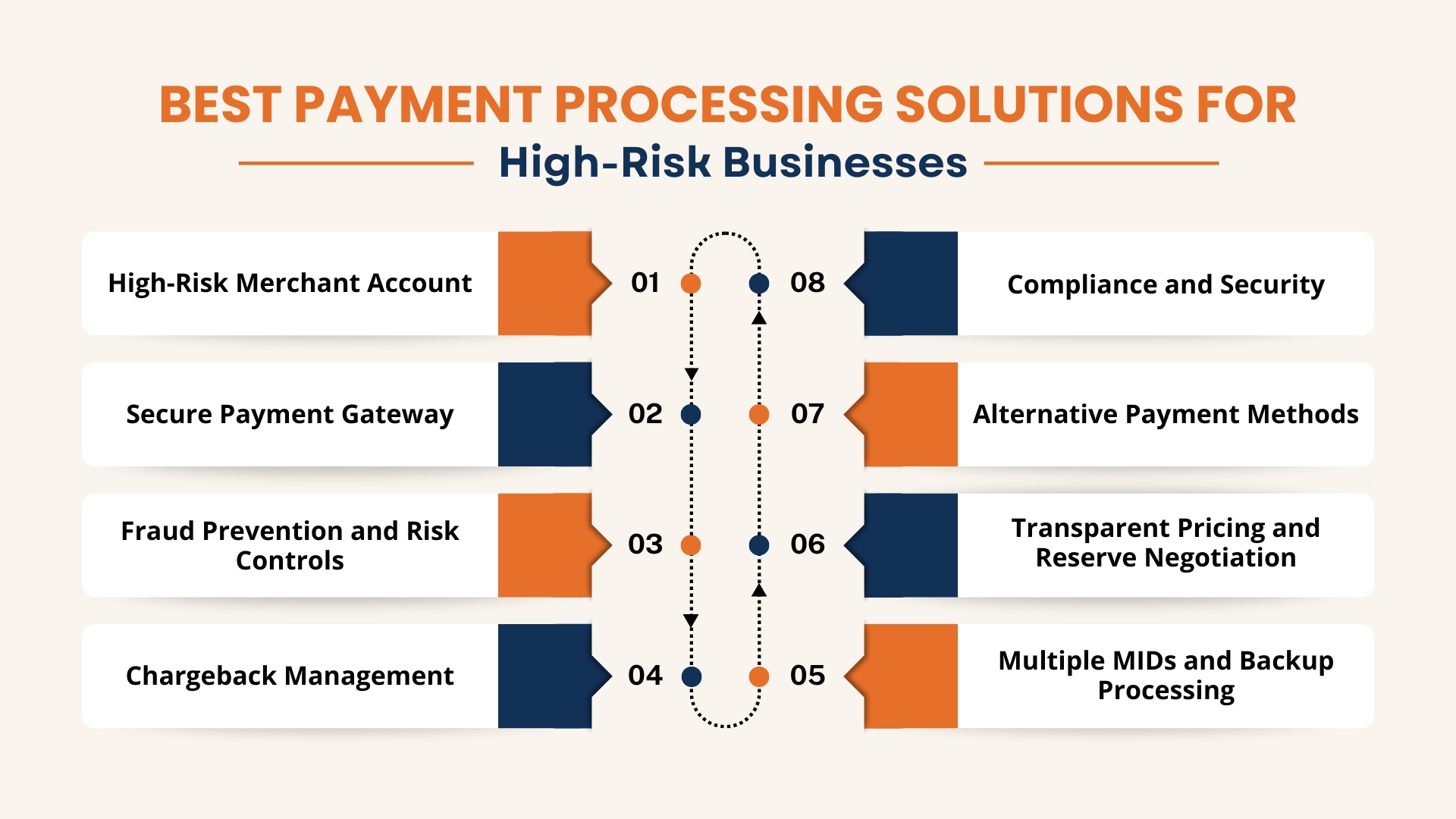

Best Payment Processing Solutions for High-Risk Businesses

1. High-Risk Merchant Account

The foundation is a merchant account designed for your industry. Businesses must not hide their business model to get approved faster. That usually creates bigger problems later.

It is essential for businesses to be transparent about the products they sell, how customers are billed, know how products or services are delivered, about your refund policy and where your customers are located.

A strong high-risk merchant account should provide realistic processing units, fair settlement terms, transparent reserves, clear chargeback rules, and support your specific industry.

The processor should understand your category rather than forcing you into a generic account that may be closed later.

Before applying it is essential for businesses to prepare their documents carefully. Your website should have clear pricing, product descriptions, refund terms, privacy policy, terms of service, contact information, fulfillment timelines, cancellation instructions, and billing descriptors.

Weak websites often create underwriting concerns because they increase customer confusion and disputes.

2. Secure Payment Gateway

The gateway should support the way your business actually sells. For eCommerce, your payment gateway should integrate with your website or cart.

For subscriptions, payment gateway should support recurring billing, retries, cart updates, cancellation flows, and customer notifications. For phone orders, payment gateway may require a virtual terminal. For in-person sales, it may need POS support.

A good high-risk gateway will provide features such as tokenization, encryption, fraud filters, velocity rules, AVS, CVV, 3D Secure, reporting, recurring billing tools, and the ability to support multiple payment methods.

The PCI DSS framework establishes a set of technical and operational security requirements which helps to protect cardholder data and is applicable to any organization that stores, processes, transmits, or otherwise impacts the security of payment information within the cardholder data environment.

For high-risk businesses, even having a flexible gateway is crucial because payment requirements can change. This lets you add new markets, new currencies, higher volume, new products, subscription offers, affiliate campaigns, or backup processors. While a rigid gateway can limit growth.

3. Fraud Prevention and Risk Controls

Fraud prevention is not optional for high-risk merchants. As fraud prevention directly affects approval rates, chargeback exposure, processor trust, and long-term account health.

Useful fraud controls include AVS checks, CVV verification, device fingerprinting, IP risk scoring, email risk checks, velocity limits, geolocation rules, transaction monitoring, 3D Secure, backlists, allowlists, manual review queues, and fraud alerts.

Key fraud prevention tools for high-risk merchants typically include Address Verification System (AVS) checks, CVV validation, multi-factor authentication, real-time fraud monitoring, and secure payment gateway infrastructure to help reduce fraudulent transactions and improve payment security.

The best fraud setup should not block every unusual order automatically. Because high strict rules can reduce approvals and also affect revenue.

Rather merchants should implement a tiered risk management approach which classifies transactions and customers on the basis of their risk level, that allows more targeted controls and enhanced fraud prevention.

Low-risk orders can be approved quickly. Medium-risk orders can trigger additional verification. High-risk orders can be declined, reviewed manually, or routed through stronger authentication.

4. Chargeback Management

Chargebacks are one of the biggest reasons high-risk merchants lose payment accounts. A good chargeback strategy begins before the dispute happens.

Use clear billing descriptors so customers recognize the charge. Send confirmation emails after purchase. Offer tracking numbers where possible. Ensure you make refund and cancellation policies easy to find.

Offer fast customer support. Respond to complaints before customers contact their bank. Keep proof of delivery, customer communication, IP logs, signed agreements, checkout records, and refund history.

Chargeback alert systems such as early dispute notifications or network-based alerts help merchants identify potential chargebacks in real time, giving them the opportunity to intervene, issue refunds, or resolve customer concerns before the dispute escalates into a formal chargeback.

For subscription businesses, chargeback prevention should include renewal reminders, easy cancellation, clear trial terms, transparent pricing, and customer self-service portals. Many disputes happen because customers forget they subscribed and do not recognize the billing descriptor, or cannot find a simple cancellation path.

5. Multiple MIDs and Backup Processing

A single MID may be enough for a small merchant, but high-volume or high-risk businesses should consider redundancy. Multiple MIDs can reduce operational risk if one account is temporarily held, capped, or reviewed.

It is also recommended to use a gateway that stores tokens independently from the merchant services provider so merchants can move more smoothly if a processor relationship changes.

It does not mean every business should immediately open several accounts. Multiple MIDs must be managed properly. Transaction volume should be managed transparently and in accordance with processor guidelines, as multiple merchant accounts are intended to support operational stability and risk management instead of hiding any chargeback activity or circumvent underwriting requirements.

6. Transparent Pricing and Reserve Negotiation

High-risk processing will often cost more than standard processing, but it does not indicate that merchants should accept unclear pricing. Rather it is essential to ask for the full cost and not the headline rate.

Businesses must review all types of fees like transaction fees, monthly fees, gateway fees, chargeback fees, refund fees, PCI fees, batch fees, cross-border fees, currency conversion fees, reserve terms, early termination fees, minimum monthly fees, and any volume penalties.

They should also conduct payment processing audits on a regular basis by analyzing transaction statements, approval percentages, chargeback ratios, and processing costs, while also discussing effective pricing structures, dispute management tools, with providers in case chargebacks levels increase.

Merchants should carefully negotiate reserve terms by understanding whether the reserve structure is rolling, fixed, limited, or temporary, clarifying the timeline for fund releases, and discussing the performance benchmarks which could cause reduced reserve requirements, while ensuring the processor provides clear justification for the reserve conditions and pathways to improved terms.

7. Alternative Payment Methods

High-risk businesses should not only depend on credit cards when other payment methods can improve flexibility, reduce risk, and improve customer convenience.

Alternative payment methods can improve customer experience, reduce card dependency, and sometimes lower certain risk exposures.

Based on the market and business model, payment options may include debit cards, ACH, eCheck, bank transfer, digital wallets, local payment methods, pay-by-link, virtual terminal payments, recurring bank payments, mobile wallets, or invoice-based payments.

High-risk businesses can also benefit by providing alternative payment methods such as mobile wallets, buy now pay later(BNPL) solutions, digital currencies, and other flexible payment solutions required to meet changing customer preferences and also reduce their dependence on a single payment channel.

The ideal payment strategy should match with the business model and customer base, because high-value B2B companies benefit from ACH and bank transfer options, international eCommerce businesses often need localized payment methods, and subscription-based services usually need recurring billing optimization and automated account updater tools.

8. Compliance and Security

High-risk merchants must take compliance seriously because payment security is not just a technical requirement rather it affects processor confidence, customer trust, and account stability.

PCI DSS is one of the most crucial standards in card payment security. PCI SSC states that PCI DSS was created to encourage and enhance payment account data security and provide a foundation of technical and operational requirements to protect payment account data globally.

Merchants should also understand industry-specific rules. CBD, financial services, gaming, tobacco, travel, debt services, and health-related products may require additional legal, advertising, age verification, disclosure, licensing, or documentation controls.

A processor that understands your industry can help you identify what underwriting will expect, but merchants should also work with qualified legal and compliance professionals whenever required.

How to Choose the Right High-Risk Payment Processor

For any businesses in a high-risk industry, selecting the right high-risk payment processor is one of the most crucial decisions.

Because the right payment provider is not just the one which offers lowest rates, rather the provider that can offer account stability in the long-term, protect cash flow, support business growth, and also provide reliable communication when risk-related problems increase.

A strong payment partner helps businesses to reduce disruptions, improve approval rates, and manage fraud and chargebacks effectively.

When evaluating a high-risk payment processor, businesses should focus on several important factors:

- Industry Experience: The provider must have experience of working with businesses in your industry and also understand the unique challenges faced by the industry.

- Transparent Pricing: All fees like transaction charges, reserves, gateway costs, compliance fees, and chargeback penalties, should be explained clearly.

- Strong Underwriting Support: A reliable provider must guide merchants through the application process and help them to prepare accurate documentation to increase the chances of approval.

- Fraud and Chargeback Protection: Businesses should look for features like AVS checks, CVV verification, 3D Secure authentication, velocity controls, blacklist management, chargeback alerts, and detailed reporting tools.

- Flexible Payment Gateway Integration: Businesses must ensure that gateways easily integrate with websites, CRMs, shopping carts, subscription platforms, APIs, or POS systems.

- Settlement and Reserve Transparency: Businesses should clearly understand payout schedules, reserve requirements, release timelines, and conditions that may trigger holds.

- Responsive Customer Support: High-risk merchants benefit greatly when they have access to knowledgeable customer support teams instead of depending only on automated systems.

Selecting a processor with strong risk management capabilities and transparent communication can highly improve long-term payment stability.

Conclusion

In today’s highly competitive digital market, for businesses operating in high-risk industries it is crucial to have reliable payment systems.

Whether your company deals with international transactions, recurring billing, digital products, high-ticket sales, or operates in highly regulated sectors having the right payment processing can impact their growth and financial stability.

Where traditional banks and standard processors often hesitate to work with high-risk merchants because of high fraud risks, chargebacks, refunds, and compliance challenges.

But, specialized high-risk payment processors can manage such complexities of high-risk merchants efficiently.

Modern high-risk merchant accounts not just help businesses to accept payments but also offer many features. They offer advanced fraud prevention systems, chargeback management tools, multi-currency support, secure payment gateways, and flexible underwriting.

This helps businesses to maintain operations smoothly while also reducing financial risks. Additionally, scalable payment technologies and alternative payment methods help businesses to grow globally and also improve customer experience with strong security and compliance.

Choosing the right high-risk payment gateway involves careful verification of fees, reserve requirements, fraud protection capabilities, industry experience, and customer support.

Businesses that focus on being transparent, and maintain low dispute ratios, and implement strong security practices are more likely to build steady processing and avoid any account disruptions.

While eCommerce, subscription services, and cross-border transactions keep growing, the demand for reliable payment processing solutions will also increase across many industries.

Partnering with experienced providers and adopting proactive risk management strategies, helps high-risk businesses to achieve secure transactions, operational continuity, and sustainable long term success in a changing global payment environment.

If you still have any query about payment processing solutions for high-risk businesses then you may book a free demo at AcePay and we are more than happy to assist you.